SK Hynix's $26.5 Billion Nasdaq Debut: A Memory Supercycle, or the Top of the Bubble?

On the day it starts trading on Nasdaq under the ticker SKHY, SK Hynix will have raised roughly $26.5 billion at about $149 per American Depositary Receipt — the biggest first-time US share sale ever by a foreign company, and the second-largest US listing of 2026 behind only SpaceX. The order book was more than 7 times oversubscribed. But the Korea-listed stock is already up around 770% in a year, and the memory industry is infamous for turning booms into busts. This piece lays out the real numbers on both sides so you can judge whether this is a supercycle or a top.

SK Hynix isn't a household name the way Nvidia is, but it sits at the exact choke point of the AI build-out: it's the world's leading supplier of high-bandwidth memory (HBM), the stacked memory that every AI accelerator needs to feed its compute. As AI demand exploded, so did SK Hynix — its Korea-listed shares have roughly quadrupled in 2026, making it the most valuable company on the South Korean exchange, ahead of even Samsung. Now it's bringing that story to US investors. The question isn't whether the business is booming. It obviously is. The question is whether you're buying near the top of a cycle that has burned investors before.

The listing by the numbers

Here's the deal itself, stripped to the essentials and set against the year's other giant offerings.

| Item | Figure |

|---|---|

| ADR price | ~$149 per share |

| Amount raised | ~$26.5 billion (some reports up to ~$29B) |

| New shares issued | ~17.79 million ADRs |

| Nasdaq ticker | SKHY |

| Oversubscription | 7x+ available shares |

| Estimated total company value | ~$1.3 trillion |

| Korea-listed 2026 gain | ~770% over 12 months |

| vs. Saudi Aramco IPO (2019) | Larger ($25.6B) |

| vs. SpaceX (June 2026) | Smaller ($85.7B) |

Two things jump out. First, the 7x oversubscription tells you demand is ferocious — US investors want direct exposure to the AI memory trade badly enough to pile into a foreign chipmaker's ADRs. Second, the $26.5 billion raise is a rounding error against a ~$1.3 trillion company; this isn't a cash-desperate raise, it's a strategic move to plant a flag in US capital markets while the AI narrative is white-hot.

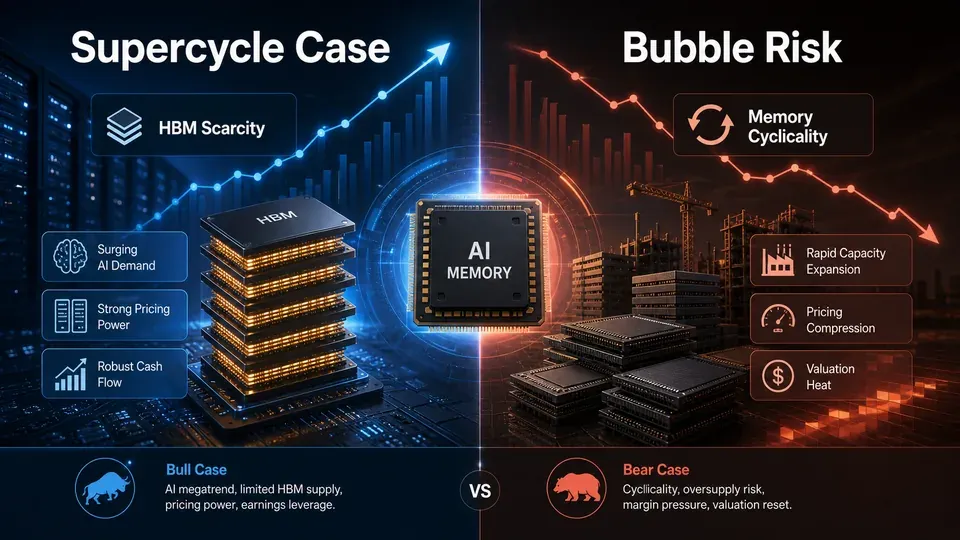

## The supercycle case: why this boom looks different

Bulls argue that this isn't 1999. The strongest points:

- HBM is structurally scarce, not just cyclically tight. Unlike commodity DRAM, HBM is hard to make, capacity-constrained, and effectively pre-sold. SK Hynix is described as "Nvidia's favorite provider" — meaning its output is spoken for well ahead of production.

- Earnings are real and beating estimates. The differentiator bulls cite versus the dot-com bubble is that memory makers are posting estimate-beating profits with buoyant guidance — this is cash, not clicks.

- Demand has a floor under it. Hyperscaler capital spending is projected to approach $1 trillion next year. Every one of those AI servers needs stacks of HBM, and there are only a handful of companies on Earth that can supply it.

- Pricing power. Because memory is the bottleneck feeding the GPU bottleneck, it captures pricing power — a dynamic we traced from the chip side in Nvidia Lost $1 Trillion in Seven Weeks — and Now Trades Cheaper Than the S&P 500, where memory names like Micron (up ~700% over the same 12 months) outran the chip designers.

The bust case: memory always breaks its own heart

Now the other side — and it's not a fringe view. Bears point to the one feature that defines the memory industry above all others: it is violently cyclical.

- Oversupply is the historical endgame. Every memory boom ends the same way — high prices pull in capacity, capacity arrives all at once, and prices crater. SK Hynix itself is planning to spend "hundreds of billions of dollars" on two new Korean plants. That's rational for the company and dangerous for the cycle, because today's shortage investment is tomorrow's glut.

- "Excessive froth." Research shop Capital Economics warns the kind of volatility now visible in these names has historically shown up mainly during bear markets — the Asian financial crisis, the dot-com bust, the Great Financial Crisis. That's not a comforting list.

- Debt is quietly rising. Across the AI supply chain, companies are funding the build-out with bonds and stock. As a cautionary marker, even SpaceX's post-IPO bonds reportedly sold off toward junk-comparable levels despite investment-grade ratings — a sign fixed-income investors see risk the equity crowd is ignoring.

- A 770% one-year move leaves no margin for error. When a stock has quadrupled, the price already assumes the good times continue. Any hint of an HBM oversupply, a hyperscaler capex pause, or a demand air-pocket can unwind years of gains fast. We walked through exactly this pattern — where the shortage itself sows the crash — in Memory-Chip Stocks Crashed During a Shortage.

## What actually decides which side is right

Everything hinges on timing the supply response. The bull and bear cases don't even disagree on the facts — HBM is scarce now, and new capacity is coming. They disagree on when that new capacity meets a possible slowdown in AI demand. If demand keeps compounding faster than SK Hynix and Micron can add fabs, the supercycle runs for years and today's $149 ADR looks cheap. If those "hundreds of billions" in new plants come online just as hyperscalers digest their spending, the classic memory glut returns and the stock gives back a chunk of that 770%.

For a typical investor, the honest reading is this: SK Hynix is a genuinely elite company at the center of the most important technology build-out of the decade — and it's a deeply cyclical stock that has already priced in a lot of good news. Analysts aren't uniformly cautious (HSBC set a price target around $166, arguing the shares could be worth ~20% more), but "great company" and "great entry point" are not the same sentence. The listing is a milestone. Whether it's a top is something only the supply curve, 12–18 months from now, will decide.

Frequently asked questions (FAQ)

What is SK Hynix and why does it matter for AI? It's a South Korean chipmaker and the world's leading supplier of high-bandwidth memory (HBM) — the stacked memory that AI accelerators like Nvidia's need to run. It sits at a genuine bottleneck in the AI supply chain.

How big is the US listing? Roughly $26.5 billion raised at about $149 per ADR (some reports put it near $29B), trading on Nasdaq as SKHY. It's the largest-ever first-time US share sale by a foreign company, behind only SpaceX among 2026 US listings.

Why do people call it a possible bubble? Because memory is famously boom-and-bust. The stock is up ~770% in a year, huge new capacity is being built, and analysts like Capital Economics warn of "excessive froth." Oversupply has ended every past memory boom.

Why do bulls think it's different this time? Real, estimate-beating earnings; structurally scarce HBM that's effectively pre-sold; and ~$1 trillion of projected hyperscaler spending underpinning demand.

Is SK Hynix bigger than Samsung now? By market value on the South Korean exchange, yes — its 2026 surge pushed it past Samsung to become the most valuable listed company in Korea, with an estimated total value near $1.3 trillion.

Key takeaways

- SK Hynix raised about $26.5 billion at ~$149/ADR on Nasdaq (SKHY) — the biggest-ever first US listing by a foreign firm, 7x+ oversubscribed.

- The Korea-listed stock is up roughly 770% in a year, making SK Hynix Korea's most valuable company (~$1.3 trillion), ahead of Samsung.

- Supercycle case: scarce, pre-sold HBM; real earnings; ~$1T of hyperscaler demand.

- Bubble case: memory always over-builds into a glut; "excessive froth" warnings; a 770% move leaves no room for error.

- The deciding variable is supply timing — when SK Hynix's "hundreds of billions" in new plants meet the AI demand curve.

How this was written AI assisted with gathering sources and structuring a first draft — fact-checking and final edits were done by a person.

References

- SK Hynix stock's US listing could signal boom—or bust — Fortune

- SK Hynix's US share sale aims to raise $26.5 billion at $149 per ADR — Reuters via Investing.com

- South Korean chipmaker SK Hynix's U.S. IPO — The Globe and Mail

- SK Hynix prepares U.S. listing at $166 per share, HSBC price target — CNBC

- Memory Chipmaker SK Hynix's US Listing Seizes on AI Demand — Bloomberg

Comments ()