Nvidia Lost $1 Trillion in Seven Weeks — and Now Trades Cheaper Than the S&P 500. Here's Why.

On July 8, 2026, Bloomberg reported that Nvidia has shed roughly $1 trillion in market value in under two months — enough to drag its valuation back to pre-AI-boom levels. The stock trades at about 18 times forward earnings, its cheapest since early 2019, and now sits below the S&P 500 (over 20x) and the Nasdaq 100 (nearly 23x). The strange part: the business isn't breaking. Nvidia still owns ~97% of the server-GPU market and analysts keep raising earnings estimates. So why is the most important company of the AI era suddenly the bargain bin of Big Tech? This piece walks through what actually happened, where the money went, and what the price reset is really telling you.

For three years, owning the AI trade mostly meant owning Nvidia. The stock soared more than 1,100% from the end of 2022 through 2025. In 2026 that script flipped. Nvidia is up just 5.6% on the year — trailing the S&P 500's 9.6% and the Nasdaq 100's 16% — while the money that used to pile into it rotated one link down the supply chain. Here's the anatomy of a $1 trillion repricing that has almost nothing to do with Nvidia's revenue.

What the numbers actually say

The headline is dramatic, but the mechanics are simple: the stock fell, the earnings didn't.

| Metric | Nvidia now (July 2026) | Context |

|---|---|---|

| Market value lost | ~$1 trillion | In under two months |

| Decline from peak | ~16% | Since all-time high on May 14, 2026 |

| Forward P/E | ~18x | Cheapest since early 2019 |

| S&P 500 forward P/E | >20x | Nvidia now trades below the market |

| Nasdaq 100 forward P/E | ~23x | And well below its own index |

| 2026 return | +5.6% | vs S&P +9.6%, Nasdaq +16% |

| Server-GPU share | ~97% | At end of 2025, barely dented |

That last row is the whole paradox. A company losing its moat gets cheap because the business is deteriorating. Nvidia got cheap while its dominance held and analysts kept lifting forecasts. When price falls but earnings estimates rise, the P/E compresses mathematically — which is exactly what a valuation reset looks like, as opposed to a fundamentals collapse.

Where the money went: one link down the chain

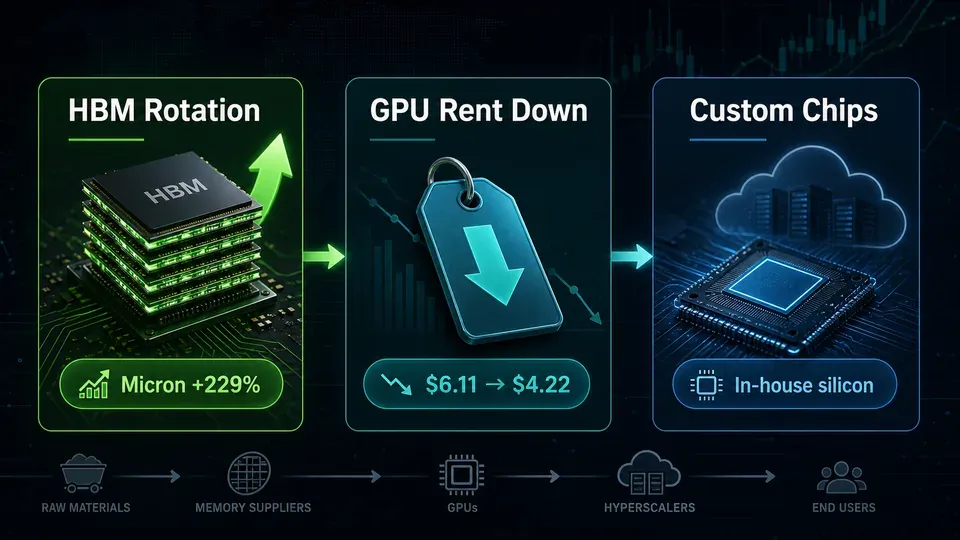

Investors didn't leave the AI trade. They rotated within it — out of the chip designer and into the chip its designs can't live without: high-bandwidth memory (HBM).

Every Nvidia AI accelerator is fed by stacks of HBM, and that memory is in acute short supply. Micron — the clearest pure-play — is up roughly 229% in 2026, with its HBM capacity reportedly sold out and prices still climbing. The logic is almost mechanical: if AI demand is real and GPUs are the bottleneck, then the memory feeding those GPUs is an even tighter bottleneck — and tighter bottlenecks get pricing power. So capital stepped "one square over" on the board, from Nvidia to its supplier.

This is the same rotation we mapped earlier from the buyer's side in The AI Money Is Rotating From Chipmakers to Hyperscalers, and it rhymes with the boom-bust pattern in Memory-Chip Stocks Crashed During a Shortage — Here's the Cycle Nobody Escapes. The through-line: in a supply-constrained AI build-out, the scarcest input wins the flows.

## Two warning signs that aren't in the P/E

A valuation reset can be a gift or a signal. Two data points suggest the market isn't only being irrational.

1. Nvidia's biggest customers are becoming its competitors. The hyperscalers that buy the most GPUs — Amazon, Google, Microsoft, Meta — are all shipping their own custom AI silicon. Every in-house chip is one fewer Nvidia chip bought. That doesn't dent 2026 revenue much, but it caps the terminal market a growth multiple is supposed to price in.

2. GPU rental prices are falling. One tracked figure: the hourly cost to rent Nvidia's flagship B200 fell from about $6.11 on May 30 to $4.22 by June 21 — roughly a 31% drop in three weeks. Falling rental rates suggest compute supply is now being built faster than new AI workloads are arriving to consume it. If that persists, it pressures the pricing power that justifies a premium multiple. (Notably, contrarian investor Michael Burry has disclosed short positions against Nvidia, Micron, and Applied Materials — a reminder the skeptics are betting real money.)

Neither point says Nvidia is a bad business. They say the easy part of the AI capex story — infinite GPU demand at premium prices — may be maturing. A market that priced Nvidia for permanent scarcity is now pricing in a world where compute is merely abundant and essential, not scarce and priceless.

## So is it cheap, or is it a value trap?

Here's the honest framing, because the data cuts both ways.

The bull case: you can now buy the company with ~97% of the server-GPU market, record revenue growth, and rising analyst estimates — for a P/E below the S&P 500. If AI compute demand keeps compounding, an 18x multiple on the category leader looks like a mispricing.

The bear case: the multiple compressed for a reason. Customer concentration is turning into customer competition, rental prices are softening, and every memory-cycle veteran knows that "sold out at record prices" is how the top of a cycle feels, not the middle. An 18x multiple isn't automatically cheap if forward earnings are about to plateau.

The useful takeaway isn't a buy or sell rating — it's that "Nvidia at its cheapest since 2019" and "Nvidia at peak cycle risk" can both be true at once. The valuation reset resolved the first question (it's no longer priced for perfection). It didn't resolve the second.

Frequently Asked Questions

Did Nvidia actually lose $1 trillion? In market value, yes — Bloomberg reported roughly $1 trillion erased in under two months as of July 8, 2026. That's a change in what investors will pay for the shares, not a loss of $1 trillion in cash or revenue.

Is Nvidia's business in trouble? Not by the numbers. It still holds ~97% server-GPU share and analysts have kept raising earnings forecasts. The decline is a valuation reset, not a fundamentals collapse.

Why is Micron up so much while Nvidia fell? High-bandwidth memory is the tighter bottleneck in the AI supply chain. Micron's HBM is reportedly sold out and prices are rising, so investors rotated from the GPU designer to its memory supplier — Micron is up ~229% in 2026.

Is 18x earnings actually cheap for Nvidia? It's cheap relative to Nvidia's own history and to the S&P 500 (>20x). Whether it's cheap in absolute terms depends on whether forward earnings keep climbing or plateau as customers in-house chips and GPU rental prices soften.

What does falling GPU rental pricing mean? The B200's hourly rental fell ~31% in three weeks (roughly $6.11 to $4.22, May 30–June 21). It suggests compute supply is outpacing new demand — an early warning on pricing power, though a single data series isn't a trend on its own.

Key Takeaways

- Nvidia shed ~$1 trillion in market value in under two months, dropping its multiple to ~18x forward earnings — its cheapest since 2019 and below the S&P 500.

- It's a valuation reset, not a fundamentals collapse: server-GPU share held near 97% and analysts kept raising estimates while the stock fell.

- Money rotated within the AI trade, not out of it — into HBM memory, where Micron is up ~229% in 2026 on sold-out capacity.

- Two real pressures on the premium: customers building their own chips and B200 rental prices down ~31% in three weeks.

- "Cheapest since 2019" and "late-cycle risk" can be true simultaneously — the reset ended the priced-for-perfection era but didn't settle the demand-durability debate.

How this was written AI helped research this piece, but every source, fact, and sentence was checked and finalized by hand.

References

- Bloomberg: "Nvidia's $1 Trillion Slide Sends Valuation to Pre-AI Boom Levels" — https://www.bloomberg.com/news/articles/2026-07-08/nvidia-s-1-trillion-slide-sends-valuation-to-pre-ai-boom-levels

- Yahoo Finance: "Nvidia's $1 Trillion Slide Sends Valuation to Pre-AI Boom Levels" — https://finance.yahoo.com/markets/stocks/articles/nvidia-1-trillion-slide-sends-084308296.html

- TIKR: "NVIDIA Stock Is Down 18% in 2026. Is the AI Leader Finally Cheap?" — https://www.tikr.com/blog/nvidia-stock-is-down-18-in-2026-is-the-ai-leader-finally-cheap

- BeInCrypto: "Smart Money is Leaving Nvidia for This AI Chip Stock" — https://beincrypto.com/nvidia-stock-institutional-money-flow-analysis/

- 24/7 Wall St.: "Michael Burry Shorts Micron, Adding to His NVIDIA and Applied Materials Short Bets" — https://247wallst.com/investing/2026/07/03/michael-burry-shorts-micron-adding-to-his-nvidia-and-applied-materials-short-bets-against-chip-stocks/

Comments ()