ASML Raised Its 2026 Forecast to €45 Billion and Jumped 6% — So Why Did Memory Stocks Fall?

ASML Raised Its 2026 Forecast to €45 Billion and Jumped 6% — So Why Did Memory Stocks Fall?

On July 15, 2026, ASML beat estimates, hiked its full-year revenue outlook for the second time this year to €43–45 billion, and its stock jumped nearly 6% to about €1,648. Yet on the same day, memory names like Micron fell around 7%, and the broader memory group is now in a bear market. This is not a contradiction — it's a signal. The very machines ASML sells are what let memory makers add supply into a tight market, and in memory, more supply means lower prices. Here's the mechanism, with the numbers.

ASML had a blowout quarter, and its stock was rewarded for it. The world's only maker of EUV lithography machines — the tools without which the most advanced chips physically cannot be produced — beat on revenue and profit, raised guidance for the second time in 2026, and announced a major capacity expansion. Shares jumped almost 6%. And yet the memory chipmakers that buy those machines fell hard the same day, with Micron down about 7% and the whole memory complex now more than 20% off its recent highs. If strong equipment demand is bullish for AI, why did the AI-memory trade sell off on the news? The answer is one of the most counterintuitive dynamics in semiconductors, and ASML's own earnings call spelled it out.

Table of Contents

- The Numbers: A Genuine Beat-and-Raise

- The Divergence: ASML Up, Memory Down

- Why Good News on Supply Is Bad News for Memory Prices

- What It Means for the Memory Trade

The Numbers: A Genuine Beat-and-Raise

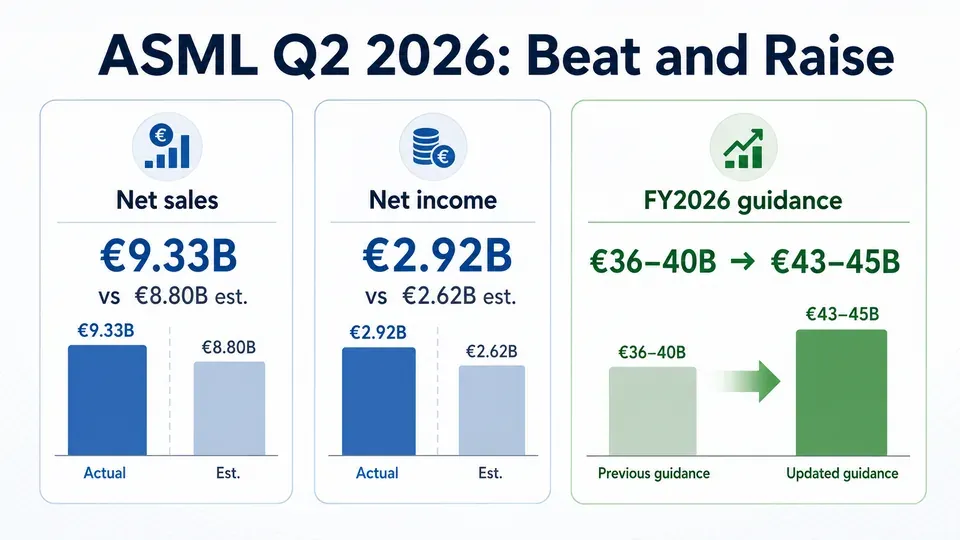

There was nothing soft about ASML's second quarter. Every headline line came in above expectations, and management lifted the full-year target.

| Metric | Q2 2026 actual | Consensus / prior | Result |

|---|---|---|---|

| Net sales | €9.33B | ~€8.80B est | Beat |

| Net income | €2.92B | ~€2.62B est | Beat |

| Gross margin | 54.0% | Above guidance | Beat |

| Systems shipped | 91 lithography systems | — | — |

| FY2026 revenue guidance | €43B–€45B | Prior €36B–€40B | Raised (2nd time in 2026) |

CEO Christophe Fouquet flagged "extremely strong" order intake driven by AI-chip demand. ASML stopped publishing a single quarterly bookings figure back in Q1 2026 — arguing that lumpy large orders distort the read on momentum — but management said order intake stayed extremely strong through the first half. On top of the raise, ASML said it plans to expand capacity by 30% in each of the next two years for both its flagship EUV tools and its DUV tools for less advanced chips. The stock closed around €1,648, up roughly 6%.

For context on why ASML sits at such a chokepoint in the supply chain, we've covered how the chip-equipment layer became a set of toll booths on the entire AI buildout.

## The Divergence: ASML Up, Memory Down

Here is the split that confused a lot of investors on July 15.

| Name | Role in the chain | Move (mid-July 2026) |

|---|---|---|

| ASML | Sells the EUV/DUV machines | ~ +6% on earnings day |

| Micron | Buys machines, makes memory | ~ −7% (July 15) |

| SK Hynix (US listing) | Memory maker | +27% post-debut Tuesday, then −10% Wednesday |

| Memory group (Micron, Samsung, SK Hynix, Roundhill Memory ETF) | The trade | all >20% off recent highs → bear market |

So the toolmaker soared while its customers sank. One of 2026's hottest trades — memory — had already tipped into a bear market, and ASML's "good" quarter did nothing to rescue it. That only makes sense once you separate two different questions: Is demand for chipmaking equipment strong? (Yes.) And Is that good for memory-chip prices? (Not necessarily — and possibly the opposite.)

Why Good News on Supply Is Bad News for Memory Prices

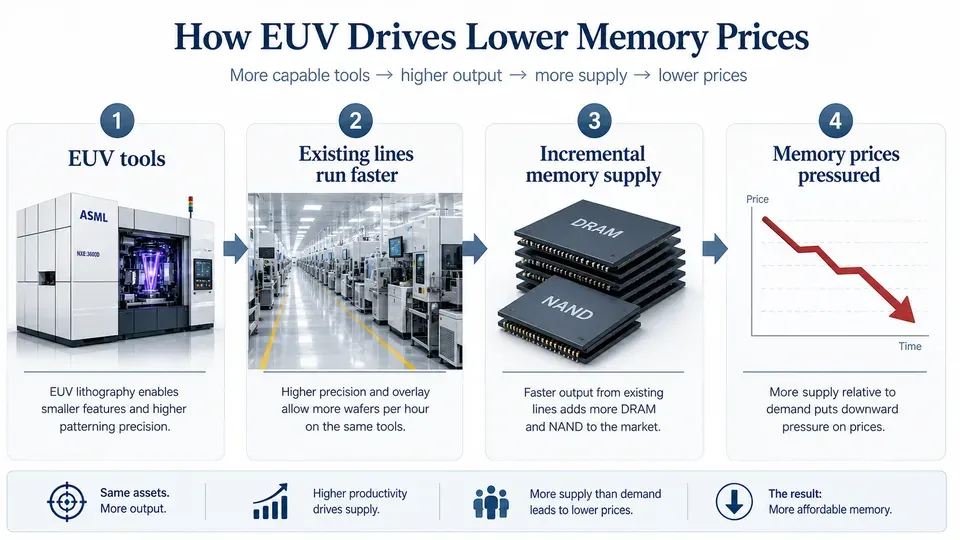

The key came from ASML's earnings call. The CFO noted that memory customers are using ASML's expensive machines to make their existing high-end production lines run faster — producing wafers more quickly than before. In other words, EUV tools aren't only about building brand-new fabs years from now; they also raise the productivity of lines that are already running.

Now layer that onto how memory pricing works. Memory (DRAM, and the HBM stacks that feed AI accelerators) is a commodity: price is set at the margin by the balance of supply and demand. The entire bull case for memory in 2026 rested on a "no new supply" story — makers holding discipline, prices staying elevated because nobody could add capacity fast. If installing ASML's machines lets producers squeeze even a little more output from current lines, that thesis cracks. In a market this tight, with prices this high, any incremental supply can push prices down. And productivity gains show up long before a new fab does.

That is why the market's logic inverts here: strong ASML demand is evidence that memory supply is about to loosen. Good news for the equipment maker reads as bad news for the commodity producer. It's the same dynamic that has burned memory investors in past cycles, where a shortage that looks permanent quietly resolves as capacity and productivity catch up — a pattern we traced in why memory-chip stocks crashed during the last shortage.

## What It Means for the Memory Trade

The takeaway isn't that ASML is a bad business or that AI demand is fading — the opposite is clearly true. The takeaway is that ASML and memory makers are exposed to different risks even inside the same AI boom. ASML sells the picks and shovels; its revenue rises with capital spending regardless of where chip prices go. Memory makers live and die by the price of a commodity, and that price is most fragile precisely when it's highest and when new tools are boosting output.

For anyone weighing the memory trade, three things matter more than the ASML headline: how disciplined producers stay on adding capacity, how fast productivity gains translate into real supply, and whether AI demand keeps growing fast enough to absorb it. Note too that memory faced a second, unrelated overhang the same week — reports of potential US export restrictions on memory products, which hit Micron directly. The ASML call didn't create the memory bear market; it removed one of the last arguments holding it up.

Frequently Asked Questions (FAQ)

Did ASML stock go up or down on earnings? Up. ASML jumped roughly 6% to about €1,648 after beating estimates and raising guidance. Some early headlines flagged an intraday dip, but the session finished sharply higher.

Why did memory stocks fall if ASML's results were strong? Because ASML's strength signals that memory makers can add supply — including by speeding up existing lines with new EUV tools. In a tight, high-priced memory market, more supply means lower prices, which is bearish for memory makers even as it's bullish for the toolmaker.

How much did ASML raise its forecast? Its full-year 2026 revenue guidance went to €43–45 billion, up from a prior €36–40 billion range — the second increase this year.

Is the memory market in a bear market? By mid-July 2026, Micron, Samsung, SK Hynix and the Roundhill Memory ETF were all more than 20% off recent highs, which is the common definition of a bear market.

Does this mean the AI boom is over? No. Equipment demand and capacity expansion point the other way. It means equipment makers and commodity-memory makers carry different risks, and memory prices are vulnerable to added supply even while AI demand stays strong.

Key Takeaways

- ASML beat on Q2 (net sales €9.33B, net income €2.92B) and raised full-year guidance to €43–45B, up from €36–40B — its second raise of 2026. Stock rose ~6%.

- On the same day, memory names fell (Micron ~ −7%), with the whole memory group now >20% off highs — a bear market.

- The reason came from ASML's own call: memory customers use its EUV machines to make existing lines faster, adding incremental supply.

- In a tight, high-priced memory market, any added supply pressures prices — so strong equipment demand reads as bad news for memory. ASML (picks-and-shovels) and memory makers (commodity) face different risks inside the same AI boom.

How this was written AI assisted with gathering sources and structuring a first draft — fact-checking and final edits were done by a person.

References

- Reuters via Rappler — ASML raises 2026 forecast, expands capacity on AI chip demand

- GlobeNewswire — ASML reports €9.3 billion total net sales and €2.9 billion net income in Q2 2026

- Seeking Alpha — AI memory, chip stocks fall again after brief recovery despite strong ASML results

- CNBC — ASML 2Q earnings: AI chip orders

- TradingKey — Micron (MU) moved down 6.96% on Jul 15

Comments ()