The AI Toll Booths: Why 5 Chip-Equipment Stocks Are Up 73% to 124% in 2026

The AI Toll Booths: Why 5 Chip-Equipment Stocks Are Up 73% to 124% in 2026

Everyone watches Nvidia. But the companies that make the machines used to build every AI chip — the "picks and shovels" of the fab — have quietly rallied 73% to 124% in 2026 on record earnings. Here is who they are, what the numbers show, and why the equipment layer behaves differently from the chipmakers.

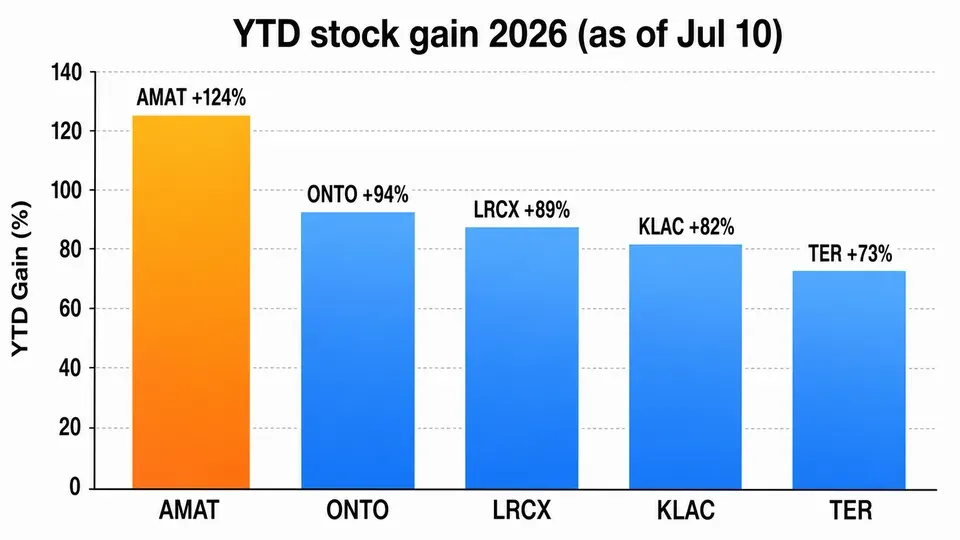

There is an old line about gold rushes: sell picks and shovels, not gold. In the 2026 AI build-out, the picks and shovels are wafer fab equipment (WFE) makers — the companies whose deposition, etch, inspection, and test machines every chipmaker must buy before a single AI accelerator ships. As hyperscaler capital spending has climbed toward roughly $800 billion, that spending flows through a small set of toll booths. Five of them just posted record results and stock gains between 73% and 124% year-to-date (as of the July 10, 2026 close). This is not a summary of one rally; it is a look at why this layer of the supply chain captures AI spending so efficiently.

Why the equipment layer is a toll booth

Chipmakers compete fiercely with each other — Nvidia versus custom silicon, one memory maker versus another. But almost all of them buy their manufacturing tools from the same handful of equipment vendors. That structure is the whole thesis:

- Every advanced node pays the toll. Whether the winning chip is a GPU, a custom ASIC, or an HBM memory stack, it is manufactured with tools from this group. The equipment makers get paid regardless of which chip design wins.

- AI geometry pulls more dollars per wafer. Gate-all-around transistors, 3D stacking, and HBM DRAM require more processing steps, more inspection, and more test per wafer than older designs — so each AI wafer spends more on equipment than a conventional one.

- It is a concentrated market. Applied Materials itself said AI adoption is expected to drive more than 80% of 2026 WFE spending growth across leading-edge foundry, DRAM, and advanced packaging. A concentrated market means pricing power.

That is why Applied Materials raised its own forecast for its semiconductor equipment business to grow more than 30% in calendar 2026, up from a prior bar of 20% just one quarter earlier — a rare mid-year upgrade that signaled the demand was arriving faster than expected.

## The five names, by the numbers

Here is the direct comparison — role in the fab, most recent reported quarterly revenue growth, and year-to-date stock move through the July 10, 2026 close. All revenue figures are company-reported for their most recent fiscal quarter.

| Company (ticker) | Role in the fab | Latest quarterly revenue | YoY growth | YTD stock (as of Jul 10) |

|---|---|---|---|---|

| Applied Materials (AMAT) | Broadest toolset: deposition, implant, CMP, packaging | $7.91B (Q2 FY26) | +11.4% | +124% |

| Lam Research (LRCX) | Etch & deposition for 3D NAND and HBM stacking | $5.84B (Q3 FY26, record) | +23.8% | +89% |

| KLA (KLAC) | Process control: defect inspection & metrology | $3.42B (Q3 FY26) | +11.5% | +82% |

| Teradyne (TER) | Automated test of finished chips | $1.28B (Q1 FY26) | +87.0% | +73% |

| Onto Innovation (ONTO) | Inspection/metrology for HBM & advanced packaging | $291.95M (Q1 FY26, record) | +9.5% | +94% |

A few things jump out. Applied Materials is the broad-exposure heavyweight; it also reported a non-GAAP gross margin near 50%, its highest in more than 25 years, on value-based pricing for differentiated tools. Teradyne shows the most explosive top-line growth — revenue up 87% with roughly 70% of it tied directly to AI demand and net income up over 300% — because testing every accelerator and HBM die is a volume that scales straight with AI shipments. KLA is the quiet monopoly-economics story: a trailing operating margin above 41%, a return on equity near 95%, and enough confidence to authorize a $7 billion buyback alongside its 17th consecutive annual dividend increase. Lam rode a record quarter on HBM stacking, guiding next-quarter revenue to roughly $6.6 billion and expecting advanced-packaging revenue to grow more than 50% in 2026. Onto is the small-cap in the group but sits at a chokepoint — inspection for HBM and advanced packaging — and locked a volume purchase agreement worth more than $240 million running through 2027 with a leading HBM manufacturer.

## What this means for an investor watching AI

The equipment layer is attractive because it is diversified across the whole chip war — but it is not risk-free, and the entry math matters now.

First, valuations have already moved. AMAT closed near a forward P/E of 36 after a 124% run; these are no longer cheap stocks. The rally has priced in a lot of the good news, so the easy gains may be behind. Second, this is a cyclical industry wearing a secular costume. WFE spending has always been boom-and-bust; the AI capex wave is real, but if hyperscaler spending plateaus, the toll booths feel it with a lag. Third, the clearest tail risk is policy: China export controls and tariffs hang over all five names, since a meaningful slice of equipment demand and supply chains touch China.

The honest framing: the "picks and shovels" logic is sound — you get paid no matter which chip wins — but sound logic at a rich price is a different bet than sound logic at a cheap one. The toll booths are collecting record tolls today. The open question is how much of that is already in the stock.

Frequently Asked Questions

What is "wafer fab equipment" (WFE)? The machines used to manufacture chips — deposition, etch, ion implant, inspection/metrology, and test tools. Every chipmaker buys them, which is why the vendors capture spending regardless of which chip design wins.

Why are these called "picks and shovels" of AI? Because they profit from the build-out itself rather than from any single chip. Nvidia, custom-ASIC makers, and memory firms all buy from the same equipment vendors, so the toolmakers get paid across the whole industry.

Which of the five is growing fastest? By reported revenue growth, Teradyne led at about +87% year over year, with roughly 70% of its revenue tied to AI demand. Applied Materials had the largest 2026 stock gain in the group at about +124%.

What is the biggest risk to this group? Policy and cyclicality. China export controls and tariffs are the shared tail risk, and WFE spending has historically been cyclical — a plateau in hyperscaler capex would hit these names with a lag.

Do I have to pick a single stock? Part of the appeal is that you don't — the group spreads exposure across deposition, inspection, packaging, and test. But each name has different valuation and concentration, so they are not interchangeable.

Key Takeaways

- The AI build-out flows through a small set of equipment "toll booths" that get paid no matter which chip design wins.

- Five of them — AMAT, LRCX, KLAC, TER, ONTO — are up 73% to 124% year-to-date on record earnings.

- AI is expected to drive more than 80% of 2026 WFE spending growth; Applied Materials raised its 2026 equipment growth forecast past 30%.

- The layer is diversified across the chip war but not cheap — valuations have re-rated, and China policy is the shared tail risk.

How this was written AI assisted with gathering sources and structuring a first draft — fact-checking and final edits were done by a person.

References

- 24/7 Wall St., "These 5 Chip Stocks Are Riding the AI Fab Spending Wave" (Jul 11, 2026): https://247wallst.com/investing/2026/07/11/these-5-chip-stocks-are-riding-the-ai-fab-spending-wave/

- Yahoo Finance, "Lam Research vs. Applied Materials: Which AI Chip Stock Has the Edge?": https://finance.yahoo.com/markets/stocks/articles/lam-research-vs-applied-materials-123000020.html

- TIKR, "Applied Materials Posts Highest Gross Margin in 25 Years": https://www.tikr.com/blog/applied-materials-posts-highest-gross-margin-in-25-years-what-the-income-statement-reveals-for-the-stock

- Yahoo Finance, "Lam Research Expects Packaging Growth of 50%": https://finance.yahoo.com/technology/articles/lam-research-expects-packaging-growth-131600390.html

Comments ()