Google Is Now Selling TPUs to Crack Nvidia's 81% Grip. Here's What Actually Changes.

Google Is Now Selling TPUs to Crack Nvidia's 81% Grip. Here's What Actually Changes.

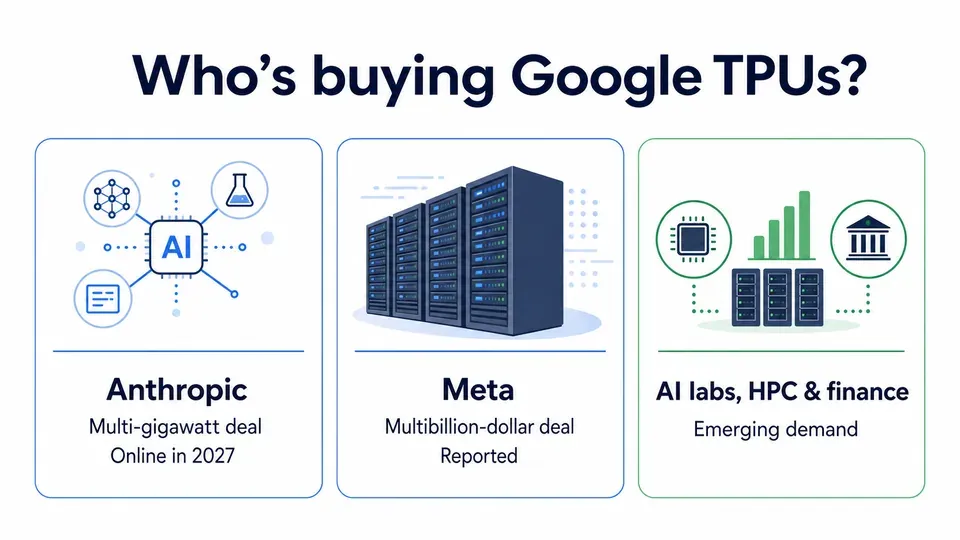

Google is shifting its Tensor Processing Units (TPUs) from a cloud-rental-only product to chips it will ship to select customers' own data centers — its most direct attack yet on Nvidia, which still controls roughly 81% of the data-center AI chip market. Anthropic has signed a multi-gigawatt TPU deal (chips online in 2027) and Meta a reported multibillion-dollar agreement. This post explains how dominant Nvidia really is, exactly what Google changed, who's buying, and why this threatens Nvidia — but slowly.

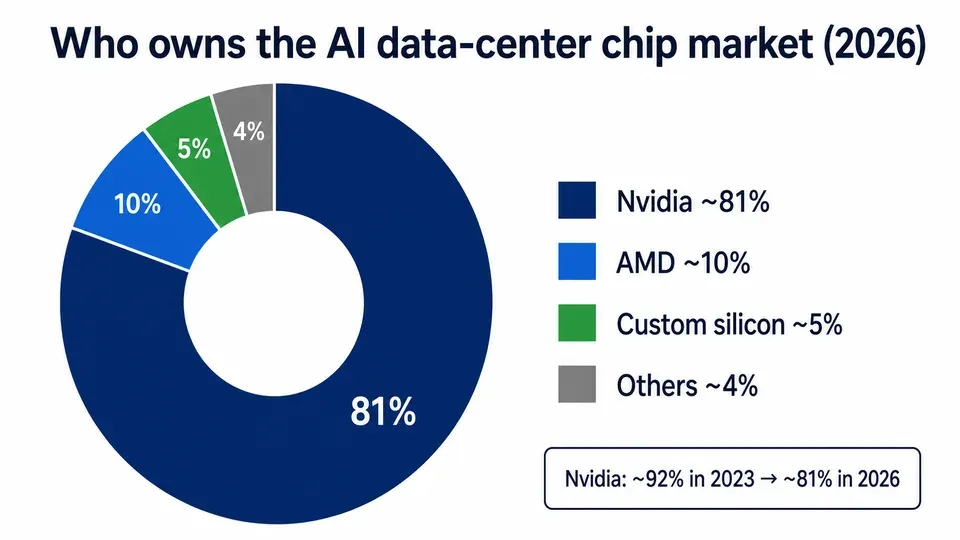

For a decade, Google's TPUs were a paradox: some of the most capable AI accelerators on earth, and you couldn't buy one. You could only rent them through Google Cloud. That is now changing. Google has begun selling TPUs to a select group of customers to run in their own data centers, turning an internal cost-saving tool into a merchant-silicon business aimed squarely at Nvidia. The stakes are enormous: Nvidia holds roughly 81% of the data-center AI chip market (some estimates run to 90%), and data-center sales make up about 90% of its revenue. Anthropic and Meta are already lined up. But dislodging Nvidia is about far more than the chip — and that's where the story gets interesting.

Table of Contents

- How Dominant Nvidia Really Is

- What Google Actually Changed

- The Customers Lining Up

- Why This Threatens Nvidia Slowly

How Dominant Nvidia Really Is

Before judging Google's move, you have to size the mountain. Nvidia's grip on AI data-center silicon is one of the most concentrated positions in modern tech.

| Metric | Figure |

|---|---|

| Nvidia data-center AI chip share (2026, IDC) | ~81% (some estimates up to 90%) |

| Share in 2023 (for comparison) | ~92% |

| AMD's share | ~10% |

| Custom silicon (Google TPU, AWS Trainium, etc.) combined | ~5% |

| Data center as % of Nvidia revenue | ~90% |

| Nvidia Q1 FY2026 revenue | $44.1B (+69% YoY) |

Two things stand out. First, Nvidia's share has slipped from about 92% in 2023 to roughly 81% — dominance, but eroding at the edges. Second, all custom silicon combined — every TPU, Trainium and in-house accelerator — still adds up to only about 5%. Google isn't attacking from parity; it's attacking from a sliver. That's the context for why even a credible challenger changes things gradually, not overnight.

## What Google Actually Changed

The shift is subtle but strategic. Until now, TPUs were GCP-only: you accessed them by renting Google Cloud capacity, and the chips never left Google's buildings. On its Q1 earnings call, CEO Sundar Pichai described the new direction directly:

"As TPU demand grows from AI labs, capital markets firms, and high-performance computing applications, we'll begin to deliver TPUs to a select group of customers in their own data centers in a hardware configuration to expand our addressable market opportunity."

Read that carefully: "in their own data centers." That's the whole change. Google is willing to let TPUs — most recently the TPU v7 generation — physically leave its cloud and run on customers' premises. It converts TPU from a feature that makes Google Cloud attractive into a product Google sells, addressing the large population of buyers who want AI compute but don't want to be locked into renting it inside one vendor's cloud. It's the difference between a hotel and a homebuilder.

This is the same competitive pressure we examined in whether custom AI chips can dethrone Nvidia — except Google's version is no longer hypothetical or internal-only. It's a chip with a price and a customer list.

The Customers Lining Up

The demand is real and already contracted. The marquee deals:

| Customer | Deal | Timeline |

|---|---|---|

| Anthropic | Multi-gigawatt agreement for next-generation TPUs | Chips coming online in 2027 |

| Meta | Reported multibillion-dollar TPU deal (per The Information) | Not fully disclosed |

| OpenAI, AI labs, HPC & capital-markets firms | Cited by Google as target demand | Emerging |

The Anthropic deal is the headline: a multi-gigawatt commitment is measured in power draw, not chip count, which tells you the scale is data-center-sized, not a pilot. Notably, the same AI labs buy from everyone — Anthropic has also signed multi-gigawatt capacity with Amazon's Trainium — because at today's demand, no single supplier can satisfy a frontier lab. That's actually part of Google's opening: Nvidia can't make enough GPUs, so buyers are actively cultivating a second and third source. Google wants to be that source.

## Why This Threatens Nvidia Slowly

Here's the part the headlines usually skip: selling a competitive chip is necessary but nowhere near sufficient to break Nvidia. Three frictions keep "still Nvidia, for now" as the industry's default answer.

- The software moat. Nvidia's real lock-in isn't the GPU; it's CUDA and the mature ecosystem of libraries, tooling and engineers built on top of it over 15 years. TPUs use a different software stack (JAX/XLA-centric). A buyer switching chips is also switching toolchains and retraining teams — a cost that has nothing to do with the silicon's raw performance.

- Merchant hardware is a new discipline for Google. Renting TPUs inside your own tightly-controlled cloud is very different from shipping chips into a customer's data center and supporting them there — firmware, servicing, supply guarantees, on-site reliability. Google is good at data centers; it is unproven at being a hardware vendor to third parties at scale.

- Nvidia isn't standing still. With ~90% of its revenue riding on data-center AI, Nvidia has every incentive and enormous resources to defend the position, and its release cadence remains aggressive.

So the realistic framing is not "Google kills Nvidia." It's that the AI-compute market is slowly shifting from a near-monopoly to a two-or-three-supplier oligopoly — and even that shift plays out over years, with the marquee TPU deployments only ramping in 2027. For buyers, the win is optionality and pricing leverage long before it's a change in who leads. For Nvidia, the threat is not a cliff; it's margin pressure and a slow ceiling on how much of the market it can keep. That's a smaller, more accurate story than "Nvidia killer" — and a more durable one.

Frequently Asked Questions

Is Google actually selling TPUs now, or still renting them? Both. TPUs remain available to rent on Google Cloud, but Google has said it will now also deliver them to a select group of customers to run in their own data centers — the key change.

How big is Nvidia's lead? Nvidia holds roughly 81% of the data-center AI chip market in 2026 (some estimates up to 90%), down from about 92% in 2023. All custom silicon combined is only about 5%.

Who is buying Google's TPUs? Anthropic signed a multi-gigawatt deal for next-generation TPUs (online in 2027), and Meta reportedly signed a multibillion-dollar agreement. Google also cites AI labs, HPC and capital-markets firms as target demand.

Why can't Google just take Nvidia's share quickly? Nvidia's moat is software (CUDA) and ecosystem, not just the chip. Switching means retooling software and retraining teams. Google is also unproven as a merchant-hardware vendor to third parties.

What does this mean for AI buyers? More leverage. Even a credible second source gives buyers negotiating power on price and supply — a benefit that arrives well before any change in market leadership.

Key Takeaways

- Google is moving TPUs from cloud-rental-only to selling chips into customers' own data centers — its most direct shot at Nvidia yet.

- Nvidia still holds roughly 81% of the data-center AI chip market (down from ~92% in 2023); all custom silicon combined is only ~5%.

- Anthropic signed a multi-gigawatt TPU deal (online 2027); Meta a reported multibillion-dollar deal.

- Nvidia's moat is CUDA and ecosystem, not the chip — switching costs, plus Google's unproven merchant-hardware muscle, slow the threat.

- The realistic outcome is a shift from near-monopoly to oligopoly over years — pricing leverage for buyers well before a change in who leads.

How this was written AI assisted with gathering sources and structuring a first draft — fact-checking and final edits were done by a person.

References

- Yahoo Finance, "Google to sell TPU chips to 'select' customers in latest shot at Nvidia": https://finance.yahoo.com/markets/stocks/article/google-to-sell-tpu-chips-to-select-customers-in-latest-shot-at-nvidia-214900221.html

- Android Headlines, "Google Wants to Challenge Nvidia by Selling Its Own AI Chips": https://www.androidheadlines.com/2026/06/google-tpu-chips-nvidia-ai-data-center-competition.html

- SemiAnalysis, "Google TPUv7: The 900lb Gorilla In the Room": https://newsletter.semianalysis.com/p/tpuv7-google-takes-a-swing-at-the

- Silicon Analysts, "NVIDIA AI GPU Market Share 2026: ~80% of AI Accelerators": https://siliconanalysts.com/analysis/nvidia-ai-accelerator-market-share-2024-2026

- BigGo Finance, "Google Declares TPU External Sales, But Data Center Industry Says 'Still NVIDIA For Now'": https://finance.biggo.com/news/fnRB950BtCxy99G5Vrr3

Comments ()