SpaceX Is Already Below Its $135 IPO Price — What a $2 Trillion Valuation and 72x Sales Really Mean

Twenty-six days after the largest IPO in history, SpaceX closed at $148 — below its $135 offer price on a first-trade basis and under the $150 it opened at on June 12, 2026. Yet the company is still worth around $2 trillion, trades near 72 times this year's projected sales, and just got fast-tracked into the Nasdaq-100. So which is it: a world-class business or a wildly overpriced one? This piece breaks down the real numbers behind the debate — where SpaceX makes its money, why the multiple is so extreme, and what the early slide is actually telling investors.

When SpaceX priced its IPO at $135 a share and opened at $150 on June 12, 2026, it instantly became the most valuable company ever to go public — raising roughly $85.7 billion in gross proceeds, the largest US IPO on record. The stock ran to a high of $201.80 on June 16. Less than a month later it slipped back under its debut price. The New York Times captured the split-screen mood in a single headline: "It's a World-Class Investment. It's a Junk Investment." Both camps are looking at the same financials. Here's what those financials actually say.

Where SpaceX's money really comes from

The first thing to understand is that "SpaceX" as an investment is mostly Starlink, its satellite-internet business — not rockets.

| Metric | Figure | Source context |

|---|---|---|

| 2025 connectivity (Starlink) revenue | ~$11.39B | ~61% of total company sales |

| Starlink 2025 operating profit | ~$4.4B | Core profit center |

| Active Starlink customers (Feb 2026) | 10M+ | Across 160+ countries/markets |

| 2026 total revenue (projected) | ~$27–30B | Analyst/consensus range |

| 2026 projected EBITDA margin | ~63% | Driven almost entirely by Starlink |

| 2026 free cash flow (segment) | ~$5B | Before heavy Starship/other capex |

The takeaway: a launch company that most people picture in terms of Falcon 9 and Starship is, financially, a subscription internet provider with a rocket division attached. Starlink is the engine; everything else is either a cost center or a bet on the future. That matters enormously for how you value the stock, because you're paying a space-exploration multiple for what is, today, largely a connectivity utility.

## The valuation math: why 72x sales is the whole argument

At roughly $2 trillion and about $25–30 billion in 2026 revenue, SpaceX trades at something like 70–80 times sales. To put that in perspective, most profitable megacaps trade in the single digits to low double digits on that measure. Even Nvidia at the peak of the AI mania was well below this on a price-to-sales basis.

A multiple that high only makes sense under one assumption: that Starlink (and eventually Starship-enabled businesses) will grow into a category-defining, near-monopoly cash machine — think "the internet backbone for the half of the planet that's still poorly connected, plus the launch layer for the entire space economy." If you believe that, 72x today's sales is just an awkward snapshot of a company whose revenue is about to compound for a decade.

If you don't believe it, the same number is the definition of a bubble. Here's the honest two-sided ledger:

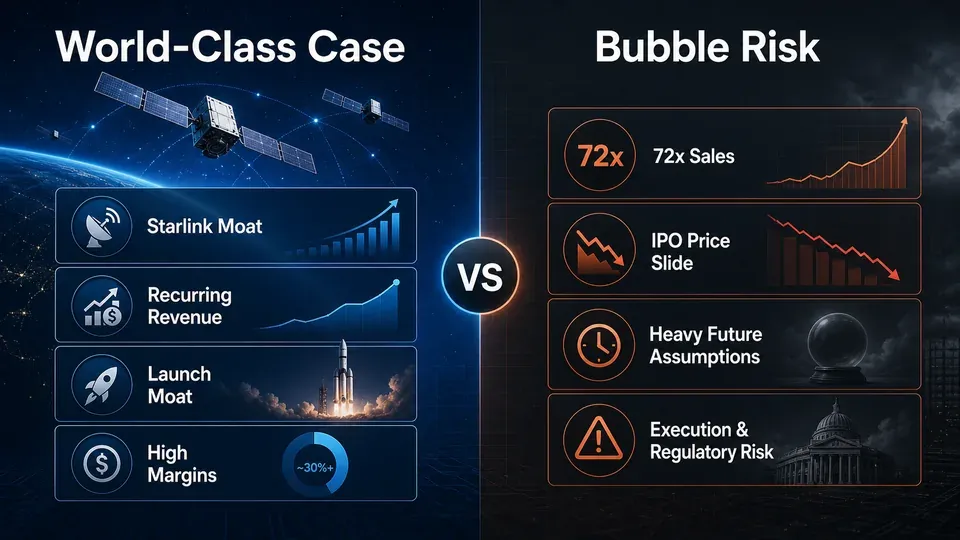

The world-class case - Starlink is already profitable and scaling fast, with a structural lead (thousands of satellites already in orbit) rivals can't quickly copy. - SpaceX owns the cheapest, most reliable launch capability on Earth — a genuine moat, not a marketing claim. - Optionality: Starship, in-space manufacturing, and even orbital data centers are lottery tickets you get for free on top of the Starlink base.

The junk-investment case - Consolidated free cash flow turns negative once you include Starship and other capital spending — Starlink's profits are effectively subsidizing the moonshots. - Elon Musk himself has warned of a "genuine risk of bankruptcy" if Starship can't hit a sustained flight cadence (roughly one launch every two weeks). - Post-IPO, SpaceX's bonds reportedly traded down toward junk-comparable levels even while carrying investment-grade ratings — a signal that fixed-income investors, who care about downside, are wary.

Why the stock fell so fast — and why the Nasdaq-100 forced it higher first

Two mechanical forces collided in SpaceX's first month.

Force one: index inclusion. SpaceX was added to the Nasdaq-100 on July 7 — less than a month after listing, thanks to the exchange's revised rules for fast-tracking large new companies. That inclusion forces every fund tracking the index to buy the stock regardless of price, which front-loads demand and can inflate the price above where active buyers would set it.

Force two: the unwind. Once that forced buying is absorbed, the price has to stand on its own. With the stock having spiked to $201.80, a pullback to $148 is less "SpaceX is failing" and more "the index-driven pop faded and reality reset in." A newly public megacap trading below its opening print within a month is a warning that the initial price was set by mechanics, not conviction.

This is the same lesson we drew about a very different space bet in AI Data Centers in Space: Why SpaceX Filed for 1 Million Satellites — with SpaceX, you're often paying today for cash flows that live a decade out, and the market's mood about that gap can swing violently.

## So how should a normal investor read this?

Strip away the theater and three facts remain true at once: SpaceX is a genuinely dominant, profitable-at-the-core business; its valuation prices in a near-flawless decade; and its early trading shows how much of the initial price was mechanical rather than fundamental. Those aren't contradictions — they're the reason reasonable people land in opposite camps.

The practical framing: at 72x sales, you are not buying today's SpaceX. You're buying a specific future — one where Starlink becomes a global utility and Starship rewrites launch economics. If that future arrives, the entry price barely matters. If it slips even a few years, a 70x-sales stock can lose half its value without the business ever "failing." The debate isn't really about whether SpaceX is a great company. It's about whether a great company can also be a bad stock at the wrong price.

Frequently asked questions (FAQ)

Did SpaceX stock actually drop below its IPO price? On a first-trade basis, yes in spirit: it priced at $135, opened at $150 on June 12, 2026, and closed at $148 on July 8 — under its opening print for a second straight day, after peaking at $201.80 on June 16.

How much is SpaceX worth now? Around $2 trillion. Reported figures cluster near a ~$1.77T IPO valuation and roughly $2.1–2.3T in early trading, making it one of the most valuable US-listed companies.

What does SpaceX actually make its money from? Overwhelmingly Starlink, its satellite-internet service — about 61% of 2025 revenue and the company's main profit source. Launch and other segments are far smaller contributors today.

Why is 72x sales considered a red flag? Because it implies flawless, multi-year growth is already priced in. Most profitable large companies trade in the single-to-low-double-digit range on price-to-sales; a 70x+ multiple leaves little room for delays or disappointments.

Is SpaceX profitable? Starlink is solidly profitable (~$4.4B operating profit in 2025), but on a consolidated basis heavy Starship and other capital spending can push total free cash flow negative.

Key takeaways

- SpaceX priced at $135, opened at $150, peaked at $201.80 (June 16), then closed at $148 on July 8 — below its debut inside a month.

- It's still worth roughly $2 trillion and trades near 72x 2026 sales — a multiple that only works if a near-perfect decade of growth arrives.

- Financially, SpaceX is mostly Starlink: ~61% of 2025 revenue and its core profit engine.

- The early slide reflects mechanics — a Nasdaq-100 inclusion pop that faded — as much as any change in the business.

- The real debate isn't "great company vs. bad company." It's whether a great company is worth this price today.

How this was written This piece was drafted with AI's research help; a human verified every fact and polished the final wording.

References

- SpaceX stock closes below debut price at $148 after Nasdaq-100 inclusion — CNBC

- SpaceX locks in IPO price of $135, largest stock debut ever — NBC News

- SpaceX is joining the Nasdaq 100. Here's what to know — CNN Business

- SpaceX is heavily reliant on Starlink for growth and profit — CNBC

- 6 Charts on SpaceX's Pre-IPO Financials — Morningstar

- Initial public offering of SpaceX — Wikipedia

Comments ()