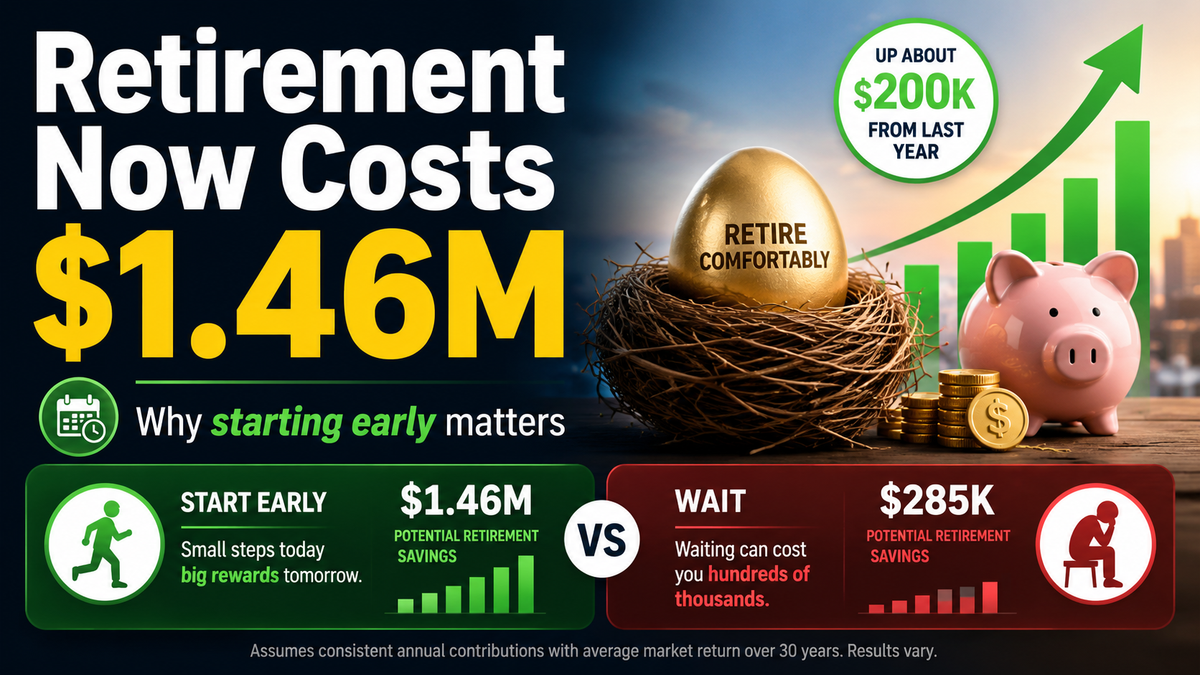

Americans Now Say Retirement Costs $1.46 Million

TL;DR — Americans now believe they need $1.46 million to retire comfortably — about $200,000 more than they thought a year ago — and half fear their savings won't last. The number keeps climbing faster than most people's balances. The fix isn't earning a perfect figure; it's understanding what's actually driving it.

The "magic number" for retirement just got bigger again. Americans now think they need $1.46 million to retire — roughly $200,000 more than last year's estimate — according to survey data reported by Yahoo Finance, and nearly half worry their money will run out before they do. At the same time, CNBC notes that IRAs hold trillions more than 401(k) plans, yet people barely contribute to them directly. There's a gap between what we say we need and what we actually do.

So what? First, understand why the number keeps rising. It's not random anxiety — it's inflation compounding into expectations. When the cost of housing, healthcare, and daily life ratchets up, the lump sum needed to fund 25–30 years of it ratchets up too. A $200K jump in one year mostly reflects that people are extrapolating today's higher prices across a long retirement. The headline figure is really a story about the cost of living, wearing a savings-goal costume.

Second, that scary number is an average for a "comfortable" retirement — not a universal toll gate. What you actually need depends on where you live, whether you carry debt, when you claim Social Security or a pension, and how you want to live. Plenty of people retire well on far less; some need far more. Treating $1.46M as a pass/fail line is the fastest way to feel hopeless and do nothing.

| The fear | The reframe |

|---|---|

| "I need $1.46M or I've failed" | It's an average for "comfortable," not a hard line |

| "The number keeps rising" | Mostly inflation in disguise |

| "Saving feels pointless" | Time + compounding beat the perfect number |

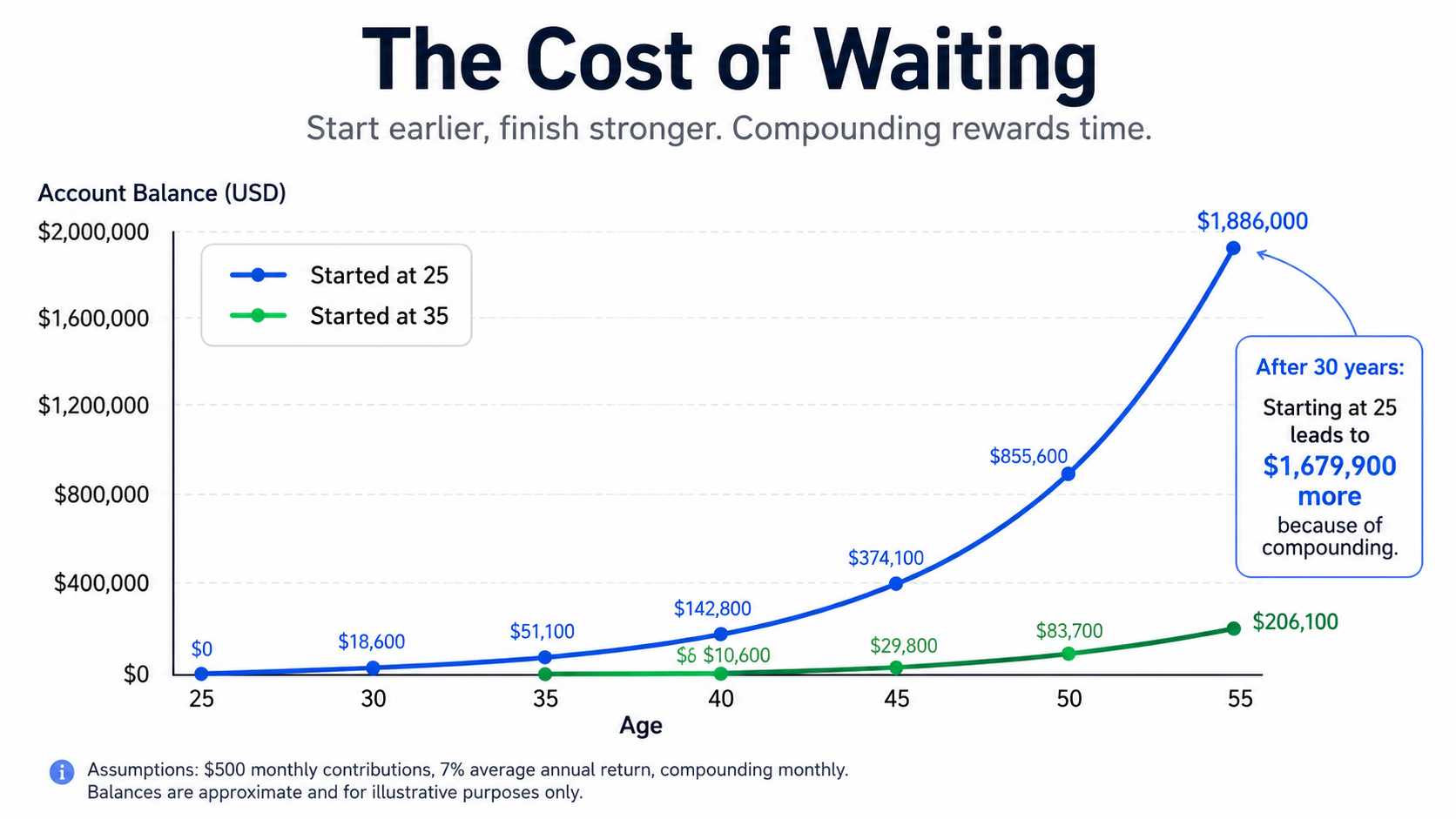

The most useful response to a rising target isn't to despair — it's to make the math work for you instead of against you. The same compounding that inflates the goal also rewards anyone who starts early and stays consistent. Someone who invests steadily from their late 20s can reach a big number with far smaller monthly contributions than someone scrambling in their 50s, simply because time does the heavy lifting. The cruelest part of the retirement gap is that it punishes delay more than it punishes a modest income.

The IRA detail is the quiet, practical lesson buried in the news. Many people pour money into a workplace 401(k) and stop there, leaving the tax advantages of an IRA on the table. Using both — and actually contributing, not just opening the account — is one of the simplest ways to chip away at that intimidating figure. The tools exist; they're just underused.

The honest caveat: survey "magic numbers" are blunt instruments. They lump together wildly different lives into one headline, and they're better at generating anxiety than plans. The right move is to ignore the scary average, estimate your actual expenses, and work backward — then automate contributions so the decision happens once, not every month.

Bottom line: The retirement number will always look terrifying in a headline — so stop staring at the average and start the boring, automatic saving that quietly makes it irrelevant.

Sources: Yahoo Finance, CNBC, June 27–28, 2026

Tags: #Finance #Retirement #Investing #PersonalFinance #Money

Comments ()