Why Traders Now See 54% Odds the Fed Hikes in 2026 — Not Cuts

Why Traders Now See 54% Odds the Fed Hikes in 2026 — Not Cuts

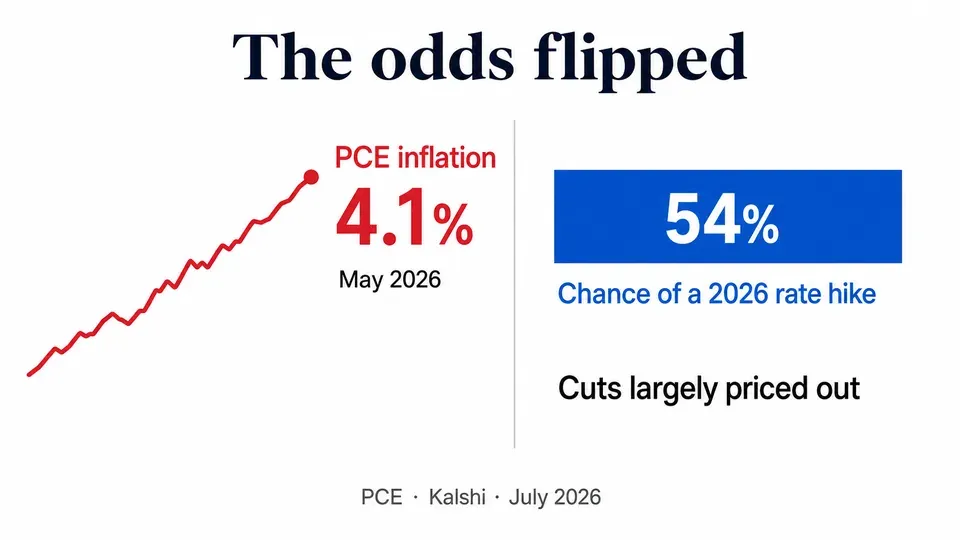

For most of the last two years the market debate was how fast will the Fed cut? In mid-2026 that flipped. Prediction-market traders now price a 54% chance the Fed raises rates this year, driven by inflation running at 4.1% and a visibly split committee under new chair Kevin Warsh. Here is why the odds turned, what "54%" really means, and what a hike would do to your money.

The conventional wisdom on interest rates just inverted. Through 2024 and 2025, nearly every forecast argued about the pace of rate cuts. As of July 2026, traders on the prediction market Kalshi put the odds of a 2026 rate hike at roughly 54% — better than a coin flip that the next move is up, not down. That is a genuinely surprising regime, and it is not coming from nowhere: inflation has reaccelerated, the Federal Reserve is openly divided, and there is a new chair in the building. This post explains what changed, how to read a "54%" market probability without over-trusting it, and what an actual hike would mean for mortgages, savings, and stocks.

What actually changed

Three things moved together, and each reinforces the others.

1. Inflation reaccelerated. The Fed's preferred gauge, the personal consumption expenditures (PCE) price index, rose 4.1% year-over-year in May 2026 — the highest annual reading since April 2023. That is roughly double the Fed's 2% target. When inflation drifts back up, the case for cutting evaporates and the case for hiking reappears.

2. The committee split in public. The June FOMC meeting minutes revealed a rare, open division. In the Fed's own words, "many participants" thought the appropriate rate by year-end would be within or slightly below the current range — while "many other participants" thought it should be above it. That is not nuance; that is the committee disagreeing about the direction of the next move. Markets hate ambiguity, and they priced the uncertainty as a near-even bet.

3. A new chair. Kevin Warsh was confirmed by the Senate (54–45) in May 2026 and sworn in as the 17th Fed chair, succeeding Jerome Powell; his first FOMC meeting was June 16. Warsh has a long-standing reputation as an inflation hawk. A hawkish chair inheriting 4.1% inflation is exactly the setup in which "hold or hike" beats "cut."

Here is the current landscape in numbers:

| Metric | Value | Note |

|---|---|---|

| Fed funds target range | 3.50%–3.75% | Unchanged since December 2025 |

| PCE inflation (May 2026, YoY) | 4.1% | Highest since April 2023 |

| Kalshi: hike in 2026 | ~54% | Better-than-even |

| Kalshi: zero rate cuts in 2026 | ~76% | Cuts largely priced out |

| Kalshi: hike before July 2027 | ~62% | |

| Kalshi: hike by 2028 | ~80% |

## What "54%" really means (and doesn't)

A prediction-market price is not a forecast from an oracle — it is the current clearing price of a bet. Read it carefully:

- 54% means "barely more likely than not." It is closer to a coin flip than to a confident call. A 54/46 split is the market saying we genuinely don't know — which is the honest answer when the committee itself is split.

- It moves daily. The same reading was 56% a day earlier. These are live prices reacting to every data point and Fed speech, not a stable prediction. A cool inflation print could push it back below 50% overnight.

- Cross-market agreement adds signal. Independent prediction market Polymarket landed near the same place — about 54% odds of a 2026 hike after Warsh's public debut. When two separate markets converge, the read is sturdier than either alone.

- The stronger signal is what's been ruled out. The most confident number here isn't the hike odds — it's the ~76% chance of zero cuts in 2026. Markets are far more sure that cuts are off the table than they are that a hike is on it. The realistic base case is "higher for longer, with a live hike risk," not "imminent hike."

In plain terms: don't read "54%" as "the Fed will hike." Read it as "the easing cycle is over, and the next move is a genuine toss-up tilted slightly toward tightening."

What a hike would actually do to your money

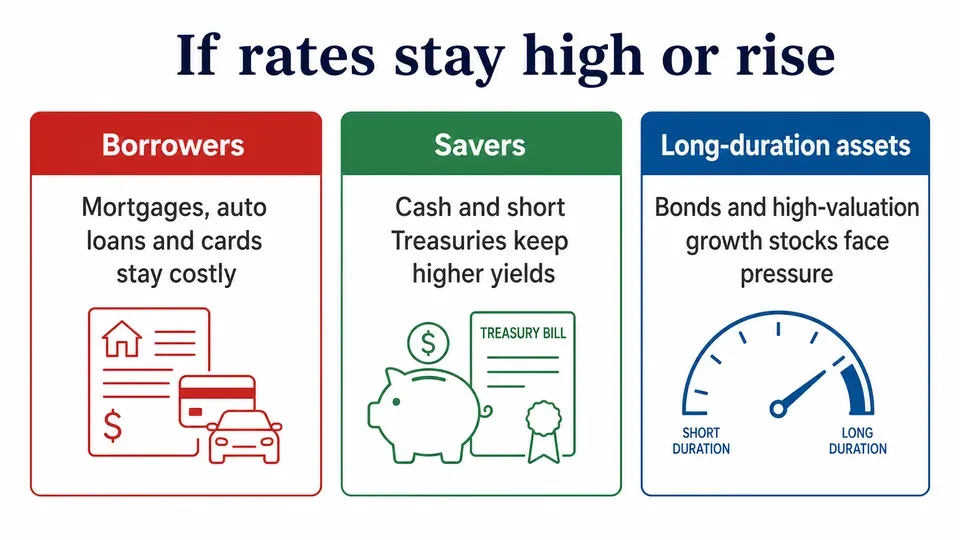

Regardless of the exact probability, the direction of risk has consequences worth planning around. If the Fed holds high or hikes:

- Borrowing stays expensive — or gets worse. Mortgages, auto loans, and credit-card APRs track the Fed's path. A hike, or simply "higher for longer," means the cheap-money era does not return on the timeline many buyers were hoping for. If you were waiting for rate cuts to refinance, that plan just got riskier.

- Cash finally pays again. The flip side: high-yield savings, money-market funds, and short-term Treasuries keep paying elevated yields. In a "no cuts, maybe a hike" world, holding cash is far less punishing than in a cutting cycle — the opportunity cost of safety drops.

- Long-duration and rate-sensitive assets face pressure. Higher-for-longer rates weigh on long-dated bonds and on the richly valued growth/tech names whose valuations lean on cheap future money. It doesn't guarantee a selloff, but it removes the "rate-cut tailwind" that markets had penciled in.

The practical posture that follows isn't panic — it's stop assuming cuts are coming. Portfolios and household budgets built on "rates will fall in 2026" are now betting against a slightly-better-than-even market. Building in the possibility of flat-to-higher rates is the conservative move.

## Frequently Asked Questions

Is the Fed definitely going to hike in 2026? No. Traders price it at roughly 54% — better than even, but far from certain. The more confident market signal is that cuts are unlikely in 2026 (~76% chance of none).

Why would the Fed hike when it was cutting before? Inflation reaccelerated. PCE hit 4.1% year-over-year in May 2026, the highest since April 2023 — roughly double the 2% target. That reverses the case for cuts.

What is the current interest rate? The federal funds target range is 3.50%–3.75%, unchanged since December 2025.

Who is Kevin Warsh? The new Fed chair, confirmed 54–45 in May 2026 and sworn in as the 17th chair, succeeding Jerome Powell. He is regarded as an inflation hawk; his first FOMC meeting was June 16, 2026.

How reliable are Kalshi and Polymarket odds? They reflect real money and update constantly, which makes them useful real-time gauges — but they are prices, not guarantees, and they swing with each data release. Convergence between the two (~54% each) makes the read more credible.

Key Takeaways

- Kalshi traders price a ~54% chance of a 2026 Fed rate hike; Polymarket is near the same level — a coin-flip tilted slightly toward tightening.

- The trigger is PCE inflation at 4.1% (May 2026, highest since April 2023) plus a publicly split FOMC.

- New chair Kevin Warsh (confirmed 54–45, sworn in May 2026) is an inflation hawk inheriting reaccelerating prices.

- The firmest signal is that cuts are largely priced out (~76% chance of none in 2026) — "higher for longer" is the base case.

- Practical takeaway: stop assuming rate cuts. Cash yields hold up; borrowers and long-duration assets bear the risk.

How this was written AI assisted with gathering sources and structuring a first draft — fact-checking and final edits were done by a person.

References

- CNBC, "Kalshi traders see roughly 50% odds of a rate hike in 2026 as Fed is split on policy" (July 9, 2026): https://www.cnbc.com/2026/07/09/kalshi-traders-see-roughly-50percent-odds-of-a-rate-hike-in-2026-as-fed-is-split-on-policy.html

- Tekedia, "Kalshi Traders See Better-Than-Even Odds of Fed Rate Hike as Policymakers Remain Divided": https://www.tekedia.com/kalshi-traders-see-better-than-even-odds-of-fed-rate-hike-as-policymakers-remain-divided/

- Bitcoin.com News, "Polymarket Bettors Set 54% Odds on a Fed Rate Hike This Year After Warsh's Debut": https://news.bitcoin.com/polymarket-bettors-set-54-odds-on-a-fed-rate-hike-this-year-after-warshs-debut/

- CNBC, "Kevin Warsh wins Senate confirmation as the next Federal Reserve chair" (May 13, 2026): https://www.cnbc.com/2026/05/13/kevin-warsh-wins-senate-confirmation-as-the-next-federal-reserve-chair.html

- Kalshi, Fed decision markets: https://kalshi.com/category/economics/fed

Comments ()